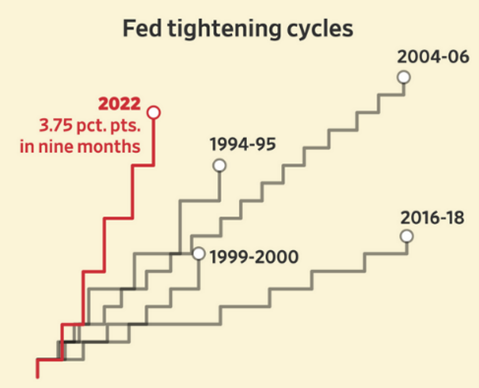

The past year has delivered lingering concerns over Covid, continued supply chain constraints, the Russian Ukraine war, unprecedented inflation, and subsequent aggressive government interest rate hikes to reduce this inflation. This crushed stocks and bonds.

A review of three broad US market sectors tells this year’s sad tale.

- The iShares Core S&P Total U.S. Stock Market exchange-traded fund (ITOT) delivered -16.9% from the end of 2021 to 16 Nov 2022.

- The iShares Core U.S. Aggregate Bond Fund (AGG) returned -12.9%.

- The proxy for the traditional 60%/40% stock/bond portfolio (VBAIX), had a -15.3%

The stock and bond markets dropped significantly in the first three quarters of 2022 and investors faced some of the most challenging return environments since the 1940’s during World War II.

The latest news from the US Federal Reserve Chairman, Jay Powell was significant in that it eased concerns about continued aggressive rate hikes (the same is expected in Canada).

Here is one of his key statements:

‘Monetary policy affects the economy and inflation with uncertain lags and the full effect of our rapid tightening so far are yet to be felt. Thus, it makes sense to moderate the pace of our rate increases as we approach the level of restraint that will be sufficient to bring inflation down. The time for moderating the pace of rate increases may come as soon as the December meeting.’

In the press conference Jay Powell said: “I don’t want to over-tighten.” This despite his previous implications that he would over-tighten.

At TriDelta we have anticipated this shift in tone for awhile believing that most of the aggressive interest rate pain is behind us. We welcomed Jay Powell’s moderate comments, as did the stock market, which abruptly rallied on the news led by Chinese and U.S. technology, biotech and other under valued sectors. This will come as no surprise to those of you who have discussed recent portfolio updates with me.

Here is a collection of current key market comments, which further support our positive outlook which we published recently:

- Goldman Sachs suggests, Some Progress, But Still an Uncertain World.

The key economic question for 2023 is whether central banks will be able to bring down inflation to more acceptable levels without a recession, or at least without a deep recession. We are reasonably optimistic, but there are substantial risks to our view.

(Goldman Sachs Economics Research 16 Nov 2022) - The S&P500 closed above the 200-day moving average for the first time in over 7 months, which is a positive sign and bodes well for further strength based on historical data (Carson Research 30 Nov 2022).

- The S&P500 is now up 13.8% in 2 months. This type of move isn’t what you see in a bear market, but rather at the start of a bull market according to Chief Market Strategist at Carson Group LLC.

- Rent prices in 93 of the largest US cities decreased last month, which is another sign that inflation is peaking (@apartmentalist).

- The stock market had already bottomed by the time inflation peaked in each of the last seven inflation cycles, which appears to be unfolding again as market move higher into Dec 2022.

- The USA Herald reported that since US central bankers launched aggressive monetary policy tightening path over the last year, the US dollar has surged. In late September, the currency was up more than 16% on the year. After this month’s sharp plunge, the dollar is up more than 10% in 2022. After hawkish Federal Reserve policy sparked a dramatic decline for the US dollar, the currency is now on pace for its most significant monthly slump since September 2010, Dow Jones Market Data shows. The implications of a weaker US dollar are significant particularly for Emerging Markets, which benefit accordingly.

- The ratio of Emerging Markets to US stocks was recently at the lowest level in 21 years and over the last 12 years the EM is up a mere 28% while the US equities have more than quadrupled.

Let’s not forget that the capital market is a place where we take a long-term view and invest in companies’ equity (stocks) or debt (bonds) to invest for the long-term future of these companies and their ability to perform over time. The old adage of ‘buy low and sell high’ is a possibility when markets bottom, and early signs appear to suggest this is unfolding right now.

Let’s not forget that the capital market is a place where we take a long-term view and invest in companies’ equity (stocks) or debt (bonds) to invest for the long-term future of these companies and their ability to perform over time. The old adage of ‘buy low and sell high’ is a possibility when markets bottom, and early signs appear to suggest this is unfolding right now.

Consider that in the year 1900 the US DOW equity index was 91, in 2000 it was over 10,000 despite two world wars, the Great Depression a couple of famines and a Cold War and this equity index still did well over time.

We believe that now is one of those generational opportunities to buy the weakness and or upgrade the quality of holdings in our portfolio, which is what I have been very busy doing for the past three months. Patience will now deliver the growth. It is self-evident that the lower the price paid, the better one’s long-term returns.

Noah Blackstein, Dynamic Portfolio Manager is another proven outperformer who smells opportunity. He points out that ‘growth’ stock valuations are at one of the lowest levels of the last two decades. In a future world of below trend economic growth, secular growth will be scarce and companies with it will be sought out and rewarded. We are incredibly enthusiastic about the long opportunities over next five years.

Jeremy Siegal, the author of the seminal Stocks for the Long Run and a professor emeritus of finance at the University of Pennsylvania’s Wharton School says, “Today’s valuations look quite attractive,” he says. “I won’t predict we’ve hit bottom, no one can, but an investor in this market may be well rewarded.”

As 2022 fades and a new year emerges, we should also take advantage to reset our life vision by developing a proper financial plan:

- How best to protect all your assets, but particularly your financial assets.

- Have a plan to ensure you will not run out of money.

- What is in place to take care of your loved ones?

- Have you considered life insurance and if you already have it, review it based on your new current situation.

A financial plan has two primary roles:

- It gives you a good understanding of the things you actually can control. And that’s a very finite set of choices: you can control how much you save, how much you spend, the timing of major events, like when you buy a house or not, when to retire etc. You can’t control investment returns, but you can choose how much risk you’re going to take.

- Secondly, it tells you how much of a safety net you have and what legacy you may leave.

My key takeaways are the following:

- In this kind of environment, focus on upgrading the quality of investments at low prices rather than when people feel good about the market and asset prices are overly inflated.

- Let us assist you with a financial plan to deliver peace of mind for your future.

- Please refer me to family or friends you feel will benefit from my investment and or planning services.

Anton Tucker, CFP, FMA, CIM, FCSI

Executive VP and Portfolio Manager

anton@tridelta.ca

(905) 330-7448