Market Overview

The headlines for the first three months of 2025 were difficult to ignore as U.S. tariffs brought about global uncertainty for investors, businesses and consumers. Not everything was as bad as these headlines may have suggested but the start of the year proved that the fortunes of the prior years’ winners can quickly change.

U.S. stocks took the brunt of the tariff negativity while many international markets outperformed. Other investment types also offered some positives. This proved good news for diversified portfolios with exposure to many different investment types, geographies, and sectors.

At the time of writing, markets are continuing to experience pain in the face of global tariffs and a deepening trade war. This has led to the sharpest downturn since the March 2020 COVID crash. If you are a regular reader of these commentaries, you know that our process does not change in the face of market uncertainty. While the future can never be known, we are comforted by our disciplined and active approach to investing which we know will serve investors well and aligns with the theme of this commentary in that “this too shall pass”.

In this review we will take the opportunity to share our thoughts on the first three months of the year and what to watch for the remainder of 2025. Key themes discussed include:

- Investors and businesses view tariffs as the top risk for 2025 and the root cause of the uncertainty surrounding a potential recession.

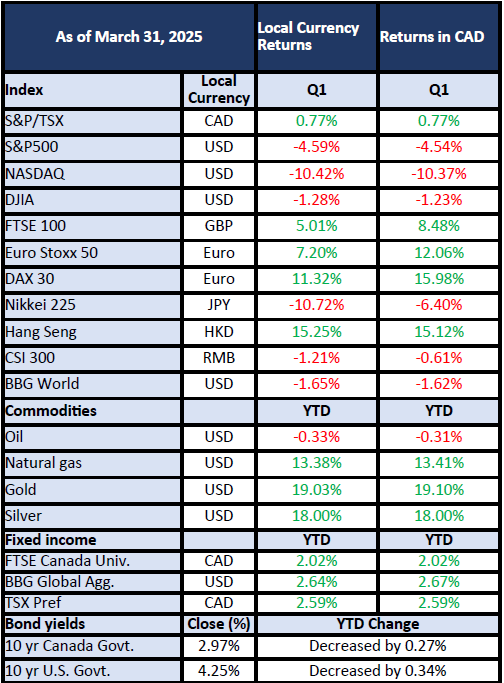

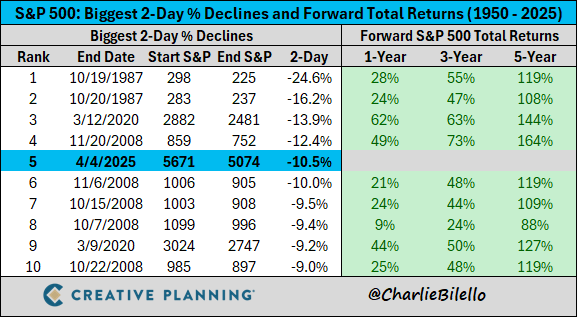

- The U.S. S&P 500 declined 10% from its February highs, marking the sixth fastest 10% fall since 1950.

- Stocks have since extended their losses into April.

- Outside of the U.S., markets with relatively lower valuations to begin the year benefited the most. Notably, Europe and China outperformed.

- Broad commodities continued their advance with sizable gains in gold given increased demand from central banks and as a hedge against current uncertainty.

- Interest rates in Canada and most of the world have trended lower while rates in the U.S. remain elevated amidst an uncertain outlook for inflation.

In this quarterly review we will be discussing several key developments, what they mean for investment decisions moving forward, and what actions we are taking to benefit client portfolios.

Tariffs and What They Mean for Investors

Investors quickly tired of the tariff back and forth, letting their frustrations be known in what ended as a broadly negative final month to the quarter as everyone awaited President Trump’s “Liberation Day” announcement April 2nd. Global markets traded lower, anticipating a 15% universal tariff on goods coming into the U.S. As we now know, the April announcement was far more aggressive than what investors and businesses were forecasting, driving global stock markets deeply into the red.

These new measures will take the U.S. effective tariff rate to its highest level in the past 100 years. Key moving forward will be the duration of these enacted tariffs, whether countries are able to negotiate exemptions or lower tariffs rates, and how consumers fare in light of rising costs. President Trump has already indicated the U.S. is open to negotiations, but we do not believe this new tariff regime will be rolled back entirely, leading to a new reality for investors, businesses, and consumers.

Likely implications of tariffs include:

- Higher inflation and lower growth: Costs on a range of goods are expected to rise, weakening the purchasing power of consumers. Global growth too, is expected to fall.

- Supply chain disruptions: Tariffs are likely to disrupt established supply chains as the U.S. and others move away from the globally integrated economy that defined the last 20 years to a more regionalized economy.

- Trade retaliation: Countries have already announced retaliatory tariffs on the U.S. which will add to the uncertainty already plaguing investors and businesses.

- Recession risk: The risk of a recession has grown but may depend on how the tariff picture evolves throughout the remainder of the year.

- Interest rates: Global central banks will need to walk a fine line between combatting persistent inflation and supporting economic growth. Interest rate decisions will depend heavily on the next several months but are likely to continue their downward trend into 2026.

The country-to-country differences in imposed tariffs are significant and require considerable thought for investment decisions.

Canada

The April announcement did not include any additional tariffs on Canada and Mexico. USMCA compliant trade is mostly protected, while goods not under this pact will be subject to 25% tariffs. The short-term negatives for Canada are apparent and we share the frustration of many Canadians but are carefully watching potential longer-term positives of the discussions being had today. These include:

- Premiers bringing down inter-provincial trade barriers may provide a small offset for rising costs elsewhere.

- Optimizing Canada’s energy for global trade is long overdue.

- Diversifying trade relationships can help open new markets for Canadian companies and add to future stability in times of geopolitical tensions.

European Union

The announced 20% universal tariff was actually within the range of what investors had been expecting and will dampen economic growth, but not all E.U. members will be impacted the same.

- The countries with the largest exports of goods to the U.S. will be the most negatively affected. This primarily includes Germany, Ireland, and Italy.

- Countries most insulated from tariffs include France and Spain.

While not in the E.U., the United Kingdom is somewhat better positioned than peers given their exports are mainly service-based.

China

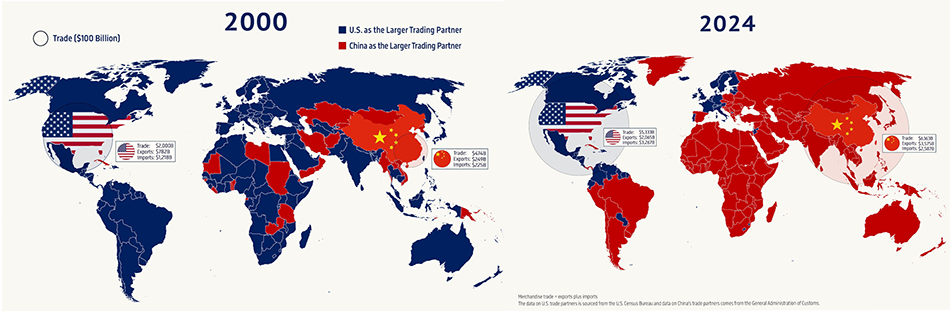

Overall tariffs on Chinese exports to the U.S. are rising to approximately 68%. Soon after, China announced retaliation measures of an additional 34% tariff on all U.S. goods. China has been a frequent target since President Trump’s first term and the recent escalation will negatively impact China in the near-term, but likely partially offset by government and central bank support. Over the longer-term it is likely we see China do additional trade in other non-U.S. markets. This has been a trend for over two decades as China has formed deep trade relations globally.

The maps below compare the year 2000 with 2024. Countries in blue are those where the U.S. is the largest trading partner. Those in red are countries with China as the largest trading partner.

What’s Next

The volatility being seen today is reminiscent of the last bout of tariff anxiety during President Trump’s first term when, in 2018, stocks fell 20% on the back of a more localized tariff policy targeting Chinese goods. While 2025 is already shaping up much differently, it may serve as a reminder that stock markets can handle bad news which, although painful, can be accounted for very quickly – like ripping off a band-aid. Then things move on. What’s been difficult this year is that the uncertainty brought on by these tariffs have clouded business and consumer behaviour leading to several more unknowns than investors are comfortable with.

We should expect markets to stabilize as trade policy begins to gain clarity and consistency, while first quarter earnings may offer reassurance that companies are prepared to navigate the new tariff landscape. Uncertainty is likely here to stay but the negativity may prove to be the best opportunity for investors since 2020. We know that declines can be painful and emotionally taxing, but they are also a healthy reality when investing and staying invested during these periods have, historically, rewarded investors over the long-term.

What We Are Doing and Why

Stocks

In previous market commentaries we have been wary of U.S. concentration. The first three months of 2025 saw significant volatility which punished the ‘winners’ of the last two years. Despite this negativity, most sectors did okay. This is most evidenced when comparing the S&P 500 with its equal-weight cousin. In Q1, the S&P 500 returned -4.59% while the equal-weight S&P returned -0.61% as investors placed a greater emphasis on valuation, income, and defensive sectors like healthcare and utilities.

- Outside of the U.S., markets with relatively lower valuations benefited the most. Notably, Europe and China outperformed.

- European stocks benefited from cheaper valuations, an increase in defense spending and manufacturing, as well as cooling Ukraine/Russia tensions (at least short term).

- Chinese momentum in Artificial Intelligence (AI) and fiscal spending helped provide a boost to Chinese stocks.

- Canada began the year positive, supported by a materials, utilities, and energy sectors. Canada’s relatively small exposure to technology stocks proved a benefit.

- The Artificial Intelligence (AI) frenzy of the prior two years has shown some cracks.

- Chinese company DeepSeek announced a significant AI advancement at a fraction of the cost many American companies had been spending.

- Despite the headlines, corporate earnings were strong and beat expectations. Investors will be closely watching forward guidance from companies to get a sense of how the consumer is faring and what actions are being taken to mitigate tariffs.

The TriDelta Pension and Growth strategies performed well to begin the year, returning 3.36% and 1.42%, respectively. The new dynamic for tariffs has meaningfully changed the outlook for 2025 but our disciplined process for investing has not. We entered the year with elevated cash levels and a more cautious approach to potential volatility. This has served us well and we intend to look at the declines being experienced in early April as an important opportunity to add longer-term value.

For an overview of how the funds stand today and our top holdings please visit our website for more information.

Learn more about our strategies:

Bonds

Investment grade Canadian bonds began the year up 2.02% with other major bond markets also positive. Bonds have been an important source of stability for diversified investment portfolios in 2025 as investors continue to benefit from elevated income yields and the prospect of additional declines in interest rates.

- Global central banks acknowledged a bleaker economic outlook in the face of global tariffs.

- The U.S. Federal Reserve held interest rates at 4.375% and are projecting two rate cuts for the remainder of 2025. Thus far, they have indicated they are not going to act early to support growth, but that may change quickly if the potential for a recession grows.

- The Bank of Canada has been more balanced in recent weeks and have not made any dramatic changes to their expectations for the year, projecting two or three more rate cuts.

- Investors are still not being adequately compensated for the risks in corporate bonds, but this is improving. At this time, investors should remain focused on high quality investment grade bonds.

- Higher inflation is here to stay and will negatively impact consumers. Concerns for a recession may rest with how businesses and consumer behaviour shifts in this new dynamic.

There are several reasons to be very active in fixed income today, regardless of whether your goal is to enhance portfolio diversification or achieve a positive return. We recommend looking outside of government bonds. Select corporate bonds, and structured notes offer meaningful advantages to building a diversified portfolio without jeopardizing overall returns.

Preferred Shares

Preferred shares continue to offer attractive yields and began the year propelled higher by redemptions, granting investors spare cash to reinvest. Later in the quarter, with less redemptions, preferreds experienced more volatility with the headlines, but noticeably outperformed equities. We expect this volatility to continue with the uncertainty being experienced more broadly in the markets for the remainder of the year and will be looking at potential declines opportunistically.

Commodities

Commodities generally had a strong start to 2025 led by gold, silver, and copper. At the time of writing, commodities have not been spared from the negativity being experienced elsewhere. The price of oil dropped to its lowest level since April 2021 given concerns over a recession reducing demand. The price of gold is down 2-3% and, in the near-term, may be an area investors look to take profits from and deploy elsewhere in investment portfolios.

Alternatives

The past few years of higher inflation and interest rate hikes created a difficult environment for many alternative investments – those not publicly traded. However, we also saw certain strategies prove their worth as their positive performance provided a counterweight to public stocks and bonds in 2022 and thus far in 2025.

Preqin, a U.K.-based data provider in the alternatives space, predicts alternatives to grow from roughly US$13 trillion in 2024 to over US$23 trillion by 2029. While the expected growth of this asset class is encouraging, it has certainly slowed more recently. Despite this, the reasons for investing in alternatives still hold true.

- Investing in alternative strategies can bring about much needed diversification through their low correlation with publicly traded stocks and bonds and offer the long-term potential for attractive returns.

TriDelta continues to seek out new opportunities for investors and recently added a fund focused on the income from music royalties. Why music royalties?

- Royalties represent stable and recurring cash flow

- Royalties last for the life of the artist plus 70 years

- Low correlation to public and private markets

It is becoming increasingly difficult to diversify portfolios using traditional asset classes. Alternative investments offer a means of reducing this volatility, enhancing cash flow, and co-investing with large institutional investors.

Celebrating 20 Years

Later this year, TriDelta will be celebrating 20 years working with clients. Our President and founding CEO, Ted Rechtshaffen, recently wrote an article in the Financial Post about the key lessons and themes he has learned from along the way.

Looking Ahead

Stock markets typically experience a sell off greater than 5% three to four times a year. Something greater than 10% is experienced once per year and a 15%+ decline usually comes every other year. Meanwhile, a greater than 20% fall happens every three to four years. At the time of writing, most major stock markets have fallen between 10% to 15%.

While the future can never be guaranteed, it is interesting to look back at previous times when markets saw sizeable losses over such a short period.

Today’s environment is one that could either generate opportunity or pull people away from their long-term goals. One of our priorities when working with clients is to help avoid the emotional investment decisions that destroy wealth. After all, the best days in the markets come after the worst days and if you wait for the good news, the market will have already moved on without you.

If you have any questions about your portfolio, our team is happy to help.